Introduction

The Lifetime Individual Savings Account (ISA) is a government-backed savings initiative introduced in the UK that allows individuals to save for their first home or for retirement, thereby encouraging a culture of saving among younger generations. With rising property prices and the need for pension provisions, the Lifetime ISA has become increasingly significant as it offers tax-free growth on investments and a government bonus. Understanding how it works and its benefits is crucial for individuals looking to secure their financial future.

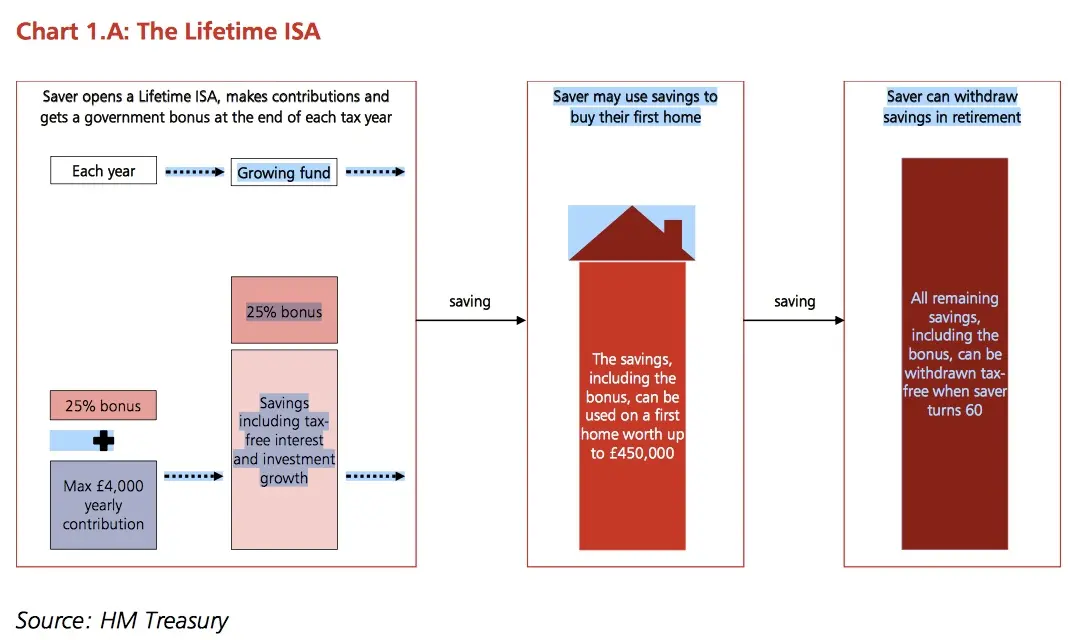

What is a Lifetime ISA?

A Lifetime ISA allows individuals aged 18 to 39 to save up to £4,000 each year until they reach the age of 50. The government contributes a 25% bonus on these contributions, effectively adding up to £1,000 per year. This means that by contributing the maximum amount each year, savers can accumulate significant extra funds to help them achieve their financial goals.

Eligible Uses

The Lifetime ISA can be used towards purchasing a first home worth up to £450,000, making it an attractive option for first-time buyers. Additionally, after the age of 60, account holders can withdraw their funds for retirement purposes without incurring penalties, ensuring it is a versatile saving tool.

Current Trends and Statistics

According to the latest data from HM Revenue and Customs (HMRC), the Lifetime ISA has seen an increase in uptake. As of April 2023, over 600,000 accounts have been opened, with contributions exceeding £3 billion since its launch in 2017. The popularity of this savings scheme highlights the increasing desire among young UK citizens to invest in their futures, be it through homeownership or retirement savings.

Considerations and Limitations

While the Lifetime ISA offers various advantages, it is essential for potential savers to be aware of its limitations. For instance, funds can only be accessed without penalty if used for a qualifying purchase or withdrawal at retirement age. If the funds are withdrawn for other reasons, there is a significant withdrawal charge of 25% on the earnings and bonuses, which can diminish the overall savings. Additionally, only one Lifetime ISA can be opened per tax year, but it can be combined with other ISA types, offering flexibility in saving strategies.

Conclusion

The Lifetime ISA presents a valuable opportunity for individuals in the UK looking to secure their financial futures, whether through homeownership or retirement savings. As the economic landscape evolves, understanding the benefits and limitations of this savings account will help individuals make informed financial decisions. The continued growth in the popularity of Lifetime ISAs suggests that as awareness increases, more individuals will look to take advantage of this financial tool to achieve their savings goals.